|

|

|

|

|

Subsequent legislation ruins Michigan's pension tax June 22, 2020

In the original pension tax legislation (Public Act 38 of 2011, effective for the 2012 tax year), there were 3 "tiers" of retirees depending on age:

It wasn't long before Public Act 597 of 2012 came along giving a larger tier 2 exemption to retirees whose pensions were from an agency not covered by the Social Security Act. The exemption is $35,000 for a single filer, $55,000 for joint filers, and $70,000 for joint filers if both spouses worked for the “uncovered” agency. The bill also added a pension exemption for tier 3 retirees not covered by the Social Security Act. Retirees born after 1952 whose age was 62-66 got a $15,000 exemption on a single return, $15,000 on a joint return and $30,000 for joint filers if both spouses worked for the “uncovered” agency. Here is the bill showing the changes. (It also exempted pensions received for services in the Michigan National Guard.)

Who are these retirees whose pensions are from an agency not covered by the Social Security Act? For the most part, police and firefighters. This is from the MI-1040 instructions, page 15:

For most local governments, police and fire pensions comprise the bulk of pensions paid, so the special exemption for retirees whose employment was not covered by the Social Security Act took a big chunk out of the savings expected from the phase-out of the pension exemption.

The idea behind the exemption for these retirees is that they they are deprived of Social Security benefits, so they need the exemption to make up the loss. But they also do not pay in to the system. The Social Security tax is 12.4% of earned income up to an annual total of $137,700, with the employee paying 6.2% and the employer paying the other 6.2%. (source) It is generally believed that the average total benefit received is more than the amount paid in, but the difference is not that great, as this story from PolitiFact says.

The other problem with deprivation of Social Security benefits argument is that it is also used to justify extra- generous pensions.

The legislature wasn't done messing with the pension tax. Public Act 149 of 2017 extended the tier 2 exemption for retirees whose pensions are from an agency not covered by the Social Security Act ($35,000/$55,000/$70,000) to tier 3 retirees, but only for those who retired as of January 1, 2013. Anyone retired after that got the $15,000/$30,000 exemption when they were age 62-66, but otherwise nothing. Here is the bill showing the changes.

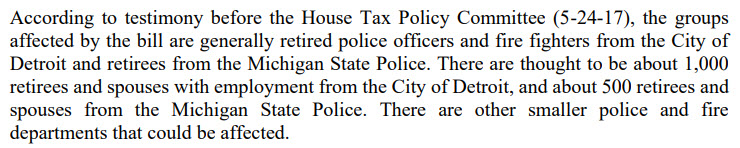

The House Fiscal Agency analysis of the bill identifies the beneficiaries of the changes:

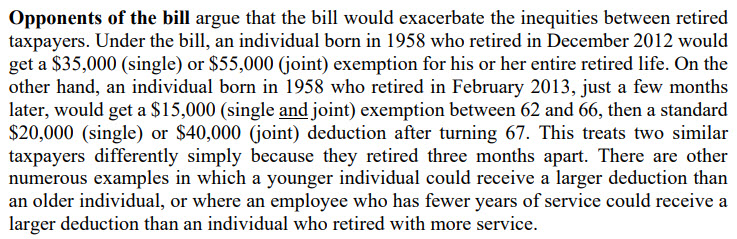

The analysis also addresses the inequities:

Not only did it treat retirees inequitably depending on retirement age, it took another big chunk out of the savings expected from the pension tax.

This chart summarizes the pension exemption:

The above chart is mine. Treasury has its own version.

Send comments, questions, and tips to stevenrharry@gmail.com or call or text me at 517-730-2638. If you'd like to be notified by email when I post a new story, let me know.

|

Public

Policy

Public

Policy